One billion dollars in emergency funds will soon be available to help homeowners "bridge" their mortgage payments while they recover from the impact of a severe income loss. The Department of Housing and Urban Development (HUD) will make the funds available to homeowners in Puerto Rico and the 32 states not covered by the Department of the Treasury's Innovation Fund for Hardest Hit Housing Markets program.

The assistance will be in the form of a declining balance, deferred payment "bridge loan" which can be used to bring mortgage, taxes and insurance payment current and make payments going forward

for up to 24 months. The funds will be provided under the Emergency Homeowners

Loan Program (EHLP), portion of the Dodd-Frank Wall Street Reform and Consumer

Protection Act and will be allocated to the individual states and Puerto Rico

based on each states proportional share of national unemployment measures as

applied to homeowners.

To be eligible for the program a household must have had an income, prior to the event which caused the delinquency, equal to or less than 120 percent of the Area Median Income (AMI) and a post-event decrease in income of at least 15 percent. The homeowners must be at least three months delinquent on mortgage payments on their principal residence and have either received a foreclosure notice or be able to self-certify to the likelihood that they will be foreclosed due to the delinquency.

The household must have a reasonable likelihood of resuming payments on the mortgage and meeting other housing expenses and debt obligations within two years. This determination will be based on a back-end ratio below 55 percent of pre-event income.

Once all arrearages are brought current, the homeowner must make monthly payments on the first mortgage based on 31 percent of the household's gross income at application. The minimum acceptable monthly payment will be $25. The balance of principal, interest, taxes, and hazard insurance will be paid by the program on the homeowner's behalf.

The assistance will be phased out over a two month period if the household's gross income at any time increases to more than 85 percent of its pre-event level and assistance will end when the household reaches either the $50,000 limit the end of the 24 month term. Other events that will terminate the assistance are a failure to report a change in employment status or income, failure to make monthly payments, or selling or refinancing the home.

The homeowner will execute a 5-year declining promissory note to HUD at the unset of the program for a declining balance, zero interest, non-recourse loan for the approximate value of the estimated assistance. The loan will be secured by a junior lien on the property. No payment will be required on the note during its 5-year term as long as the homeowner maintains the property as a principal residence and keeps the first mortgage current. If these conditions are met, the balance of the loan will decline by 20 percent annually until the note is extinguished and the junior lien is released.

At all states of the program "underwater" homeowners will be encouraged to explore participation in short sale or short-refinancing programs offered by their servicers and/or the federal government.

HUD will administer the program either by delegating some administrative functions or by channeling the funds through state housing finance agencies (HFAs). Delegated entities will be required to perform outreach, intake, eligibility screening, and counseling; a fiscal agent will be assigned to manage and distribute funds. HUD will provide information that identifies pockets within each of the designated states that have suffered the most from recent spikes in unemployment and/or mortgage delinquencies and will encourage the use of program dollars in these hardest-hit areas. The Department intends to begin taking applications from eligible homeowners by the end of the year.

Below are the complete guidelines as published by HUD...

HERE is the HUD release

---------------------------------------------------

There will be a dual delivery approach for program administration. The first approach will delegate some of the program administrative functions to designated third parties. The second approach will enable state housing finance agencies (HFAs) that operate substantially similar programs to engage in relief efforts on behalf of residents of their state.

1. Program Administration -- Delegated approach: HUD will delegate key program administration functions to separate external entities, while retaining program monitoring, compliance and long term note management functions internally. Delegations include:

Counseling Intermediary to Perform Intake, Eligibility Screening, and Outreach. HUD will enter into a cooperative agreement with NeighborWorks® America to have nonprofit housing counselors who are part of the National Foreclosure Mitigation Counseling Program administered by NeighborWorks® America to provide intake and outreach services.\

- Intake services shall include: (i) developing and disseminating program marketing materials, (ii) providing an overview of the program and eligibility requirements, (iii) conducting initial eligibility screening (including verifying income), (iv) counseling potential applicants, including providing information concerning available employment and training resources, (v) collecting and assembling homeowner documentation, (vi) submitting homeowner application, and (vii) providing transition counseling to explore with the homeowner other loss mitigation options, including loan modification, short sales, deeds-in-lieu of foreclosure, or traditional sale of home.

- The counselors shall also be encouraged to conduct outreach to entities in local communities to provide information on assistance available to unemployed homeowners through this program and shall publicize the list of entities approved to assist potential applicants with applying to the program.,

- Fiscal Agent to perform funds control, payment distribution, and note processing functions. HUD will also to contract with an entity which has extensive loan servicing and funds control capabilities to provide general accounting and fiscal control services, including collecting payments from borrowers, distributing payments to servicers on a monthly basis, performing accounting, managing loan balances, and providing payoff information. The fiscal agent would also provide note processing function and services for the program such as recording liens, storing the note and handling the payoffs at the end of the program. Once the note/ mortgage is placed and the homeowner’s final balance is determined, the loan servicing function will be transferred to HUD FHA for longer term management.

2. Program Administration -- Substantially similar state law approach: State HFAs that operate loan assistance programs that are determined by HUD to be substantially similar to the EHRF program will receive allocations to fund emergency loans for borrowers in their states as well as payments to cover the administrative costs of performing the intake and housing counseling and fiscal agent functions (described above) directly or indirectly through subcontracts with third parties.

Allocation of Program Funds

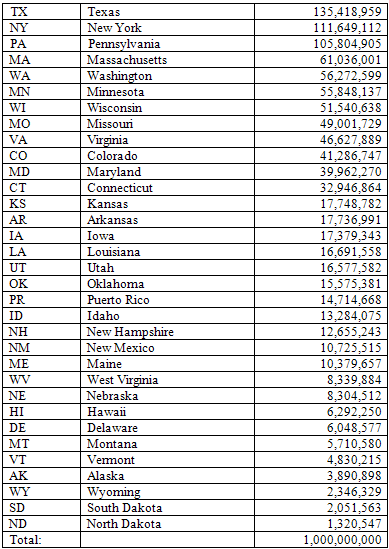

- Recipient Geography: HUD will assist borrowers living in Puerto Rico and the 32 states otherwise not funded by Treasury’s Innovation Fund for Hardest Hit Housing Markets program.

- Allocation Amount: An allocation amount will be reserved to assist homeowners living in each of these states. The total amount reserved will be based on the state’s approximate share of unemployed homeowners with a mortgage relative to all unemployed homeowners with a mortgage (See attached allocation list).

- Targeting Funds to Local Geographies: HUD will provide information that identifies pockets within each of the designated states that have suffered the most from recent spikes in unemployment and/or mortgage delinquencies. HUD will encourage the use of program dollars in these hardest-hit areas.

Homeowner Eligibility and Program Operation

Income Thresholds: Has a total pre-event household income equal to, or less than, 120 percent of the Area Median Income (AMI), which includes wage, salary, and self-employed earnings and income.

Significant Income Reduction: Has a current gross income that is at least 15 percent lower than the pre-event income.

Employment type: Both wage and salary workers and self-employed individuals are eligible.

Delinquency and Likelihood of Foreclosure: Must be at least three months delinquent on payments and have received notification of an intention to foreclose. This requirement can be documented by any written communication from the mortgagee to the homeowner indicating at least three months of missed payments and the mortgagee’s intent to foreclose. In addition, the homeowner can self-certifiy that there is a likelihood of initiation of foreclosure on the part of their mortgagee due to the homeowner being at least three months delinquent in their monthly payment.

Ability to Resume Repayment: Has a reasonable likelihood of being able to resume repayment of the first mortgage obligations within 2 years, and meet other housing expenses and debt obligations when the household regains full employment, as determined by:

- The homeowner must have a back-end ratio or DTI below 55% (principal, interest, taxes, insurance, revolving and fixed installment debt divided by total gross monthly income). For this calculation, gross income will be measured at the pre-event level.

Principal Residence: Must reside in the mortgaged property as principal residence. The mortgaged property must also be a single family residence (1 to 4 unit structure or condominium unit).

Creation of HUD Note: After the first assistance payment is made on behalf of the homeowner, the fiscal agent will create an open-ended “HUD note” and a mortgage to be in the name of the Secretary HUD of sufficient size to accommodate the expected amount of assistance to be provided to homeowner.

Ongoing Qualification of Homeowner

Termination of Monthly Assistance: Assistance is terminated and the homeowner resumes full responsibility for meeting the first lien mortgage payments in the event of any of the following circumstances:

- The maximum loan ($50,000) amount has been reached;

- The homeowner fails to report changes in unemployment status or income;

- The homeowner’s income regains 85% or more of its pre-event level;

- The homeowner no longer resides in, sells, or refinances the debt on the mortgaged property; or

- The homeowner defaults on their portion of the current first lien mortgage loan payments.

Income re-evaluation: After initial income verification at application intake, the homeowner shall be required to notify the fiscal agent of any changes in the household income and/or employment status at any point throughout the entire period of assistance.

Forms of Assistance

Use of Funds for Arrearages: On behalf of the homeowner, the fiscal agent shall use loan funds to pay 100% of arrears (mortgage principal, interest, mortgage insurance premiums, taxes, hazard insurance, and ground rent, if any).

Homeowner Payments: Homeowner contribution to monthly payment on first mortgage will be set at 31 percent of gross income at the time of application, but in no instance will it be less than $25 per month.

Use of Funds for Continuing Mortgage Assistance: The fiscal agent will make monthly mortgage payments to the servicer of the first lien mortgage in excess of the payments made by the homeowner.

Duration of Assistance: If at any time the household’s gross income increases to 85% or more of its pre-event level, assistance will be phased out by the fiscal agent over a two month period. In any event, assistance with monthly payments may not continue beyond 24 months.

Repayment Terms

Transition Counseling: The designated counseling agent shall contact each homeowner that is approaching the last months of program eligibility and remains un/underemployed (3-6 months before the assistance ends) and require the homeowner to meet with a HUD approved counseling agent to explore other loss mitigation options, including loan modification, short sales, deeds-in-lieu of foreclosure, or traditional sale of home.

Repayment of HUD Note: Following the last payment on behalf of the homeowner, the fiscal agent will process the homeowner’s “HUD Note” and record a mortgage with a specific loan balance. The note and mortgage will be in the form of a five year declining balance, zero interest, nonrecourse loan, and the mortgage shall be in the form of a secured junior lien on the property.

Terms for Declining Balance Feature: No payment is due on the note during the 5 year term so long as the assisted household maintains the property as principal residence and remains current in his or her monthly payments on the first mortgage loan. If the homeowner meets these two conditions, the balance due shall decline by twenty percent (20%) annually, until the note is extinguished and the junior loan is terminated.

Events Triggering Note Repayment: The homeowner will be responsible for repayment of the applicable balance of the HUD note to the fiscal agent or its successor, if, at any time during the five year repayment period, any of the following events occur:

- The homeowner no longer resides in the mortgaged property as a principal residence, but maintains ownership;

- The homeowner defaults on its portion of the current mortgage; or

- The homeowner receives net proceeds from selling or refinancing debt on the home. Net proceeds -- after paying outstanding applicable brokers fees, first balances (and second lien balances, as applicable), and an allowance of $2,000 to the homeowner for relocation expenses when the home is sold -- will go towards paying down the HUD note. In the event that proceeds of a sale or loan refinance are not sufficient to repay the entire HUD note, the remaining applicable balance of the HUD note shall be considered to have been met, and the lien against the property shall be released.

Provisions for Underwater Homeowners: At all stages of the program, “underwater” homeowners will be encouraged to explore participation in short sale or short refinancing programs offered by their servicer and/or the federal government (i.e. Home Affordable Foreclosure Alternatives) , which will not trigger repayment of the HUD note.

Borrowers living in the following jurisdictions are eligible to receive funds....