There has been a lot of focus in recent years on two topics; the gradual but steady decline in the homeownership rate and the huge Millennial generation, those born between the early 1980s and the earliest years of the 21st Century. There is a nexus of the two of course as there is no group in which the decline in homeownership been greater than among Millennials, now at the prime age for buying their first homes. The homeownership rate of households headed by 25 to 34-year-olds was 36.9 percent in 2014, almost 10 points below where it was in 2006, at the peak of the housing bubble.

In the current edition of its Housing Insights, Fannie Mae looks at the homeownership patterns of the Millennial generation, but does so through a different lens than usual. This is important, the company's Director of Strategic Planning, Patrick Simmons says, because the decline in the young-adult homeownership rate "has been associated with several housing market shifts, including low shares of first-time home buyers and suppressed starter home construction."

Simmons says the data has continued to show moderate declines in homeownership for young adults, but this analysis has relied on the traditional way of looking at the generation, the age group, for example, persons aged between 25 and 34 years. This, he says, doesn't portray the dynamic nature of homeownership. Instead, Fannie Mae undertook an analysis by birth cohorts (i.e. those born between 1982 and 1991. This allows not only comparing two groups of people at two points of time, it also tracks changes for the same group as they grow older and pass from one age group to the next. Cohort analysis can help determine if Millennials have started to buy homes at a faster pace as the economy has recovered and are closing the gaps with earlier generations.

Using the Census Bureau's American Community Survey (ACS), Fannie Mae looked at homeownership changes by both age groups and birth cohorts over very short periods of time. The big ACS sample enables analysis of characteristics over short intervals for successive, non-overlapping birth cohorts, which in turn allows cutting history into short intervals, in this case: 1) the end of the 2000s housing boom and economic expansion (2006-2008); 2) the housing bust (2008-2010 and 2010-2012); and 3) the early housing recovery (2012-2014), thus isolating changes during the housing recovery from change during the pre-crisis and crisis periods. Fannie used two-year wide age groups and birth cohorts and tracked homeownership rate changes over two year intervals.

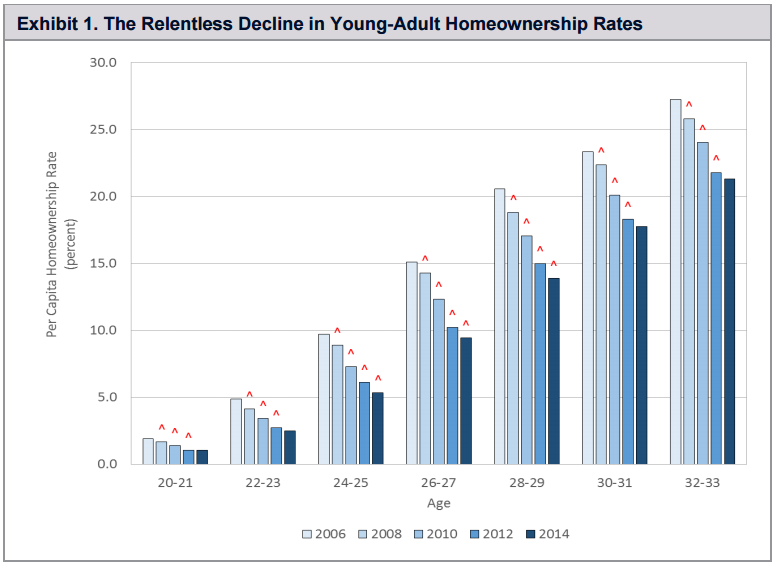

Analysis by age group (Figure 1) shows homeownership continuing to fall among young adults during the initial years of recovery but at a moderating pace. In each two-year period between 2006 and 2012 per capita homeownership rates declined for adults between the ages of 20 and 33. This continued over the next two years but the declines were neither as large nor as widespread, being statistically significant only for the groups between 24 and 29. There was no sign of an upturn however.

Simmons calls the moderating decline among age groups promising but hardly suggestive of the beginning of a recovery.

Analysis by birth cohort provides more definitive indications of a rebound however, showing gains as young adults age through their late twenties and early thirties The traditional analysis of homeownership rates by age group reveals that young-adult homeownership continued to fall during the initial years of the housing recovery, albeit at a moderating pace. However, the cohort analysis shows significant acceleration in homeownership as Millennials aged through their late twenties and early thirties during the early housing recovery. This signals that the oldest Millennials are beginning to close the gap with their predecessors. In Exhibit 2, the left-most bar for example shows that the cohort which was 20-21 in 2006 increased its per capita homeownership rate by about 2.2 percentage points as it aged to 22-23 years old in 2008.

This pattern of aging into homeownership slowed dramatically as the housing crisis in 2008 moved into recession in 2010. For those aging between 24-25 and 26-27, homeownership from 2008 to 2010 grew less than 3.5 percentage points, a point less than in the cohort that age two years earlier. These birth cohort gains continued to decrease between 2010 and 2012, but the loss moderated and for those in their late 20s and early 30s, homeownership rate gains largely stabilized. Between 2012 and 2014 the deterioration ceased for almost all age transitions. For those Millennials who aged between 28-29 and 30-31, the gains during the early recovery period were twice as large as they were for the predecessor cohorts during the housing bust, and even significantly larger than it was for the cohort passing through this age range between 2006 and 2008.

So what are the implications. Simmons said that while Millennials have homeownership rates today that are substantially lower than young adults prior to the housing bust and Great Recession these gaps are not immutable. The generation can play catch-up with prior generations as economic and housing market conditions improve. Looking at homeownership data through a cohort analysis allows researchers to see the beginnings of such a rebound and indeed we are seeing signs "of incipient recovery in young-adult homeownership demand." This in turn could signal greater demand for starter homes, more affordable purchase mortgage products, homeowner education and counseling, and other services and technologies suitable for young home buyers.

He calls signs of accelerating Millennial homeownership between 2012 and 2014 particularly notable given the headwinds they faced during the early housing recovery. Labor market conditions had begun to improve but young adults still had substantially higher unemployment compared to the pre-crisis period and credit conditions were very tight. Both of these factors have improved since 2014 - the last year for which the ACS data is available - and some changes to mortgage finance have occurred - so there is more recent support for first time homeownership. There is also a statistical issue in that immigration has begun to rebound from recession levels. Because immigrants tend to arrive here during early adulthood, and don't have high homeownership for a while after arrival, increased immigration has likely dragged down young-adult homeownership rates.

Simmons concludes that, although the improvements in the labor market and credit access since 2014 should boost Millennial homeownership demand, the tight inventories and rapid price appreciation, especially in the lower home price tiers, are reducing first-time home buyer affordability. The should highlight the importance, he says of continued industry efforts to provide housing and mortgage products to meet the growing demands from potential young home buyers.