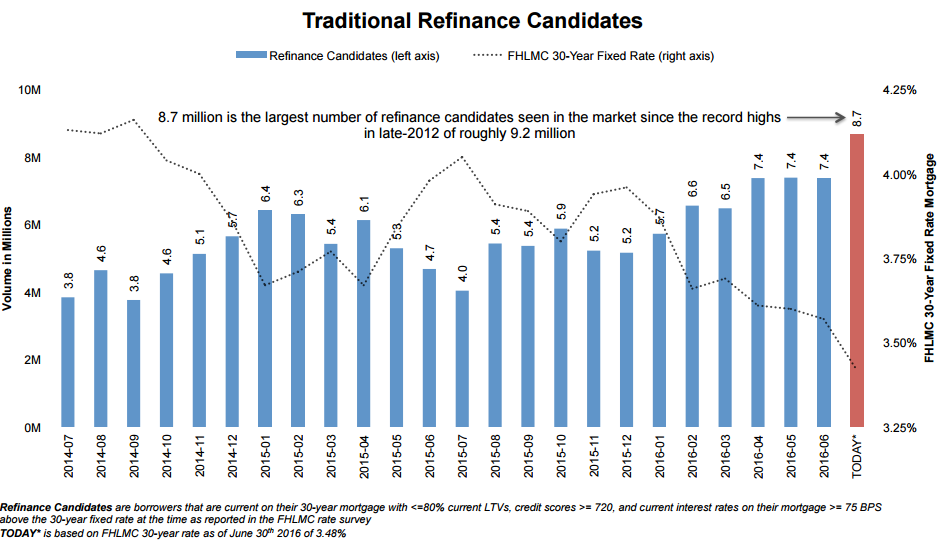

The "Brexit Effect" is the focus of Black Knight Financial Service's current Mortgage Monitor. The report, covering June mortgage performance data, notes that the aftershocks from the United Kingdom's vote to leave the European Union have resulted in an increase in the numbers of "refinanceable" homeowners to the largest pool since late 2012.

Mortgage interest rates, driven by a surge of investors running to the safety of sovereign notes globally, including those of the U.S. Treasury, have declined by about 15 basis points (bps) post-Brexit, but this, Black Knight says, has been enough to increase the number of refinance candidates by about 1.3 million to a pool of 8.7 million borrowers. Even prior to the vote in late June there were roughly 1 million more potential refinancers than when interest rates were at their lowest in early 2015; however, refinance originations and prepayment speeds in the early part of this year, the company says, have hovered well below last year's levels.

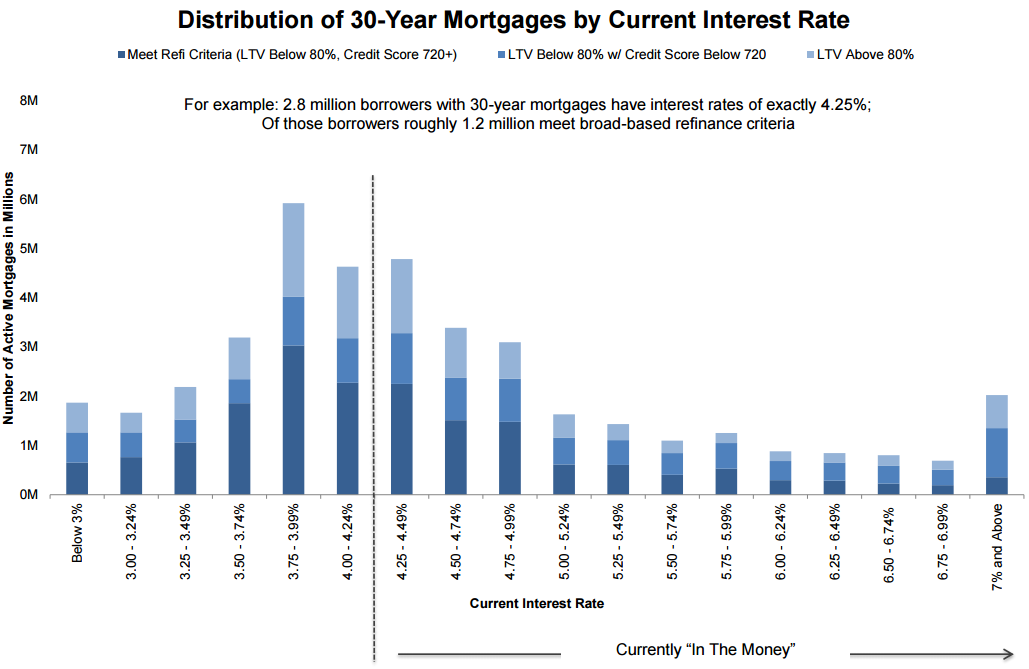

About 18.5 million borrowers, 45 percent of those with a 30-year mortgage, have a current interest rate between 3.5 and 4.5 percent and 25 percent (9 million) have rates between 4 and 4.5 percent. The "Brexit effect" and its 15 bps drop push 2.8 million borrower sitting right at 4.25 percent "into the money." Black Knight estimates that over 1.2 million of these meet broad-based eligibility criteria -- loan-to-value ratios of 80 percent or less, credit scores of 720 or higher and are current on their mortgage payments.

The company says it used a 75 bps point cut off to represent an interest rate refinancing incentive but that, with rates at the time of its analysis below 3.5 percent there may be a portion of borrowers with current rates between 3.75 and 3.99 that have an incentive as well. As an example, a 25 bps reduction in rates would save $40 a month on a $300,000 mortgages but if, by refinancing, the borrower could also eliminate mortgage insurance premiums that would substantially increase the incentive.

When the Monitor did a similar analysis of refinance candidates in March it found that 66 percent of refinance candidates could have both likely qualified for and had incentive to refinance in the spring of 2015, but for whatever reason didn't do so. Now Black Knight Data & Analytics Executive Vice President Ben Graboske says, "Unlike the 66 percent (of those borrowers), the vast majority of these new candidates did not have such incentive last year. This has produced a nearly 50 percent increase in the number of borrowers with newfound incentive to refinance, which may well be creating a more pronounced impact on refinance applications and originations as these borrowers rush to take advantage."

In the current rate environment, the effect of even slight declines in mortgage interest rates have proven to have far-reaching impact on the refinanceable population. However, the Monitor notes that there has been much less impact than one might think on home affordability.

Graboske said, "At the same time, the 55 bps reduction in rates we've seen over the first six months of this year would normally have done a great deal to increase home affordability ratios. All else being equal, the monthly mortgage payment on the average-priced home should be approximately $63 less per month than it was at the end of 2015. The post-'Brexit' decline alone would have decreased that payment by about $15 per month. However, as home values continue to appreciate - at a 5.4 percent annual rate according to the most recent Black Knight Home Price Index report - the bulk of mortgage savings are being offset by rising prices.

"Purchasing a median-priced home today requires roughly 21 percent of the median household income; much less than at the height of the bubble, and below the 2000-2002 average of 26 percent. What we need to keep an eye on is what would happen if and when interest rates begin to rise again - especially if sustained low rates continue to fuel home price appreciation as they have. Even if prices stay flat - unlikely as that is - a one percent rate increase would push affordability to 24 percent, while a two percent rate increase would put affordability well above the 2000-2002 average. The question becomes, what is a sustainable ratio in a market where Qualified Mortgage lending is the norm and student loan and other non-mortgage-related debt is on the rise?"

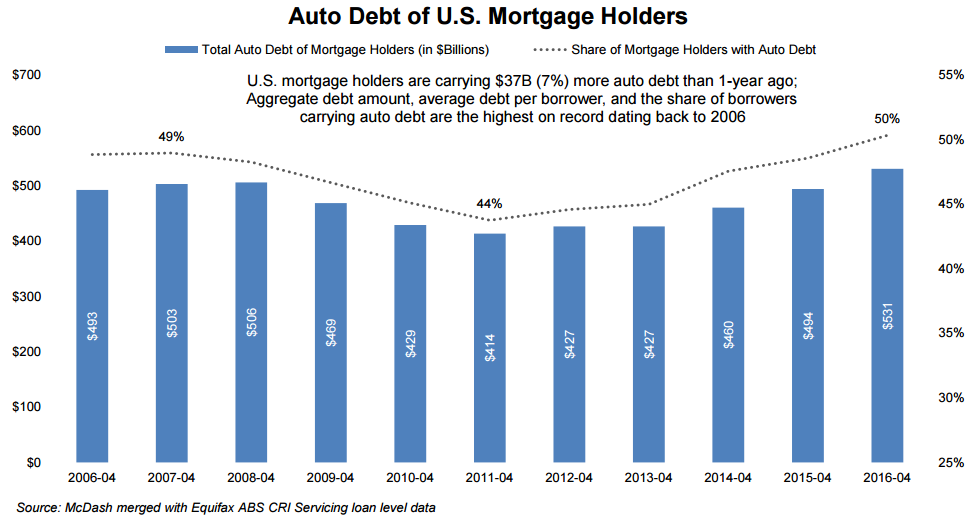

To attempt to answer that, Black Knight merged credit bureau data with its loan-level mortgage database to determine the level of auto loan debt among U.S. mortgage holders. It found that the aggregate debt amount ($531 billion), average debt per borrower ($20,500) and the share of borrowers carrying auto debt (50 percent) are all the highest on record, dating back to at least 2006. While total outstanding balances on auto loans are up nearly 30 percent from 2011 and average debt per borrower is up by nearly 20 percent, extended financing terms and low interest rates mean the average monthly payment is up only 5 percent or $25 per month and, at an average of $575, is actually lower than it was in 2007 and 2008

The combined mortgage performance and credit data shows that borrowers who are seriously delinquent on their auto debt (90 or more days past due) are eight times more likely to be behind on their mortgage payments as well, a stronger correlation to delinquency than Black Knight saw last month with regard to student debt delinquencies. However, borrowers with auto debt in good standing actually have lower non-current mortgage rates than borrowers without, with 4.5 percent of the former being delinquent on their mortgage payments, as opposed to 5.8 percent for the latter.