Real residential investment subtracted from GDP in the second quarter of the year to the greatest extent since the third quarter of 2010. Fannie Mae's August Economic Developments notes a 6.8 percent annualized decline, but the company's economists expect that sector's contribution to rebound in the third quarter.

Residential investment was only part of the GDP story with the first half of the year now complete. Fannie Mae had forecast growth of 2.1 percent on an annualized basis in its previous forecast, but midyear saw growth of only 1.9 percent. There should be a slight improvement in the second half of the year, the economists but are holding to their earlier whole year forecast of 2.0 percent.

Risks to their forecast are called roughly balanced. On the upside, consumer spending may not weaken as much as was predicted while the weakening of the dollar could boost exports more than anticipated, although trade policy muddies those waters. Downside risks include a technical default if Congress fails to raise the debt ceiling and a partial government shutdown if they don't pass a spending bill before September 30.

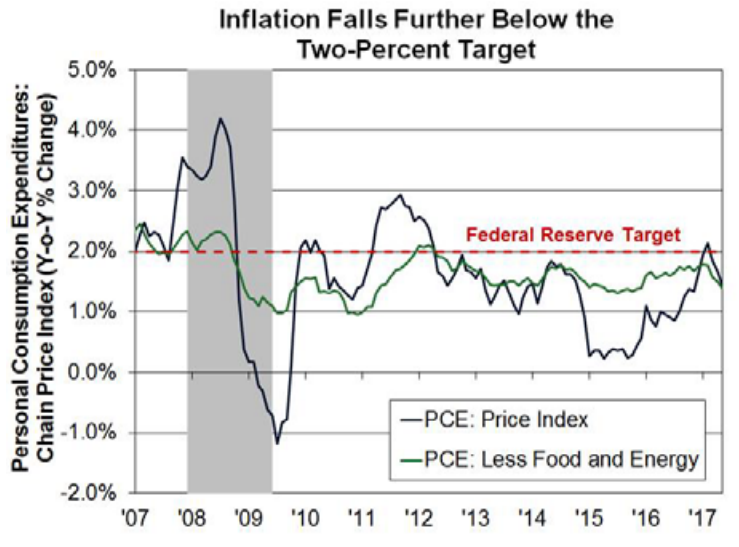

Fannie Mae does not see any sense of urgency on the part of the Federal Reserve to raise interest rates; inflation has fallen even further away from the Fed's target 2.0 percent goal. The annual increase in its favorite indicator, the Personal Consumption Expenditures Deflator, was flat in June, slowing the annual growth from 1.5 percent to 1.4 percent. It had been running at 2.2 percent in February. The Fed has still not announced a start-date for its balance-sheet tapering, but Fannie Mae is looking for that to begin next month and to December for the next rate hike.

Other housing news includes an apparent stabilizing of the homeownership rate after a decade of decline. The second quarter rate came in 0.8 percent higher than a year earlier, at 63.7 percent and was the second consecutive quarter for a year-over-year gain. Millennials appear to be moving into homeownership; the rate for the under-35 age group helped with the stabilization, rising 1.2 percent since the second quarter of 2016.

The rental vacancy rate rose for the fourth consecutive quarter to 7.3 percent, the highest since the third quarter of 2015. The homeowner vacancy rate fell to 1.5 percent, the lowest since the first quarter of 2001.

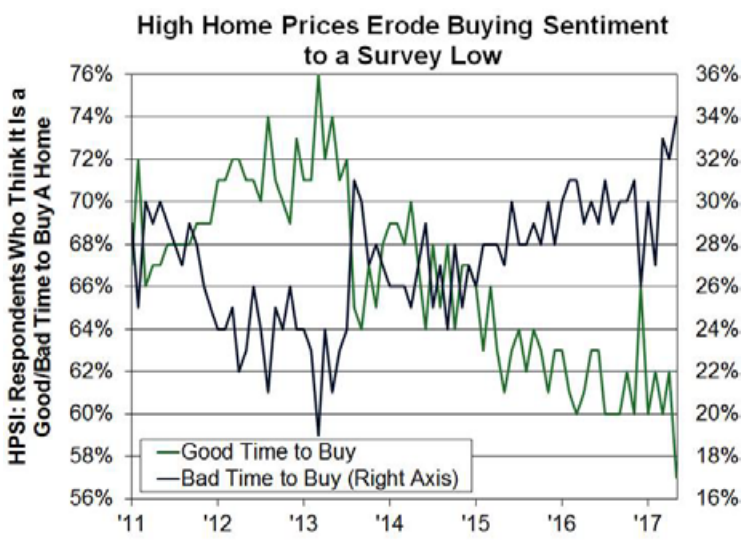

Inventories of for-sale homes continued the two-year slide that has constrained sales and boosted home prices. Fannie Mae's Home Purchase Sentiment Index fell 1.5 percentage points, reflecting, in part, a sharp decline in consumers who view the present as a good time to either buy or sell. The deterioration in "good time to buy" sentiment appears driven by concern over high home prices.

The economists call the near-term outlook for home sales "mixed." Pending sales rose in June after slipping for three straight months, and posted an annual increase for the first time since March. Pending sales echoed a stronger volume of purchase organizations in June, but those dropped in July, offsetting the June gains.

Interest rates are expected to remain near current levels, supporting home sales. The average rate is expected to be 4.0 percent in the fourth quarter. The expectations for mortgage originations are largely unchanged, although refinancing is higher than anticipated. Total single-family mortgage originations are expected to drop about 19 percent this year to $1.67 trillion and the refinancing share expected to drop 11 points to 37 percent. Overall originations will drop again in 2018, down about 6 percent to $1.57 trillion. The decline in refinancing originations next year, a 26 percent share is expected, will outweigh an increase in purchase originations.