Equity futures are modestly higher this morning as investors anticipate the latest developments from Greece as well as three key domestic data releases.

“Optimism that a new bailout for Greece is near is providing a modest boost to equity markets and weighing on the US$ index,” said economists from BMO Capital Markets. “The package is rumored to include a further €24 billion in austerity measures (about 10% of Greek GDP).”

Key Events Today:

8:30 ― The National Bureau of Economic Research refused to say recently whether the economy had exited the recession, but it should be broadly agreed upon once GDP advances for the third straight quarter, as it is expected to do in this report. First-quarter growth is anticipated to rise 3.4% following the 5.6% gain in the fourth quarter and 2.2% increase in the third quarter. The positive headline should be bolstered by strong retail sales, but held back by weak inventory growth.

“Inventories added 3.8 percentage points to fourth-quarter growth, and we think they will add 0.9 percentage point to first-quarter growth,” said analysts at IHS Global Insight. “Final sales growth should improve to 2.3% from 1.7%, with consumer spending (up 3.5%) leading the way.”

The analysts also pointed towards improvement in business equipment and defense spending, while foreign trade should be a small drag as imports rise faster than exports.

“The big drag on growth will come from construction ― residential, nonresidential, and state and local construction activity should all show sharp declines,” they added. “Since the message from most high-frequency indicators is that the economy gained momentum as the first quarter progressed, the second quarter should see stronger growth than the first.”

9:45 ― The Chicago Business Barometer, a measure of manufacturing and services in the Midwest, is expected to post growth for the seventh consecutive month in April. After dipping slightly to 58.8 in March ― a score well above the 50-marker of growth ― the index should return to above 60.0, where it stood in the first two months of the year. In addition to strong new orders in March, a forward looking component, forecasts are optimistic in part because the Empire State and Philadelphia indexes each improved this month.

“A rise in April’s data would be one of the first indications of economic growth as we transition into the second quarter of 2010,” said economists from BBVA.

10:00 ― The week should end on a fairly positive note with the Reuters/U of Michigan report Consumer Sentiment sentiment report posting a slight increase in April. Preliminary results earlier in the month saw the index shed a few points from 73.6 to 69.5, but recent retail results suggest a return to 71.0 in the final results.

“The setback in early April was attributed to disappointment with healthcare reform legislation,” said economists from IHS Global Insight. “An improving labor market, generally favorable economic news and more positive readings from the housing market should help to put the sentiment index back on an upward path.”

In yesterday’s session, stocks gained steadily throughout the day and withstood some pressure in the final hour of the trading. The Dow closed 122 points higher and the benchmark S&P 500 finished 15 points higher.

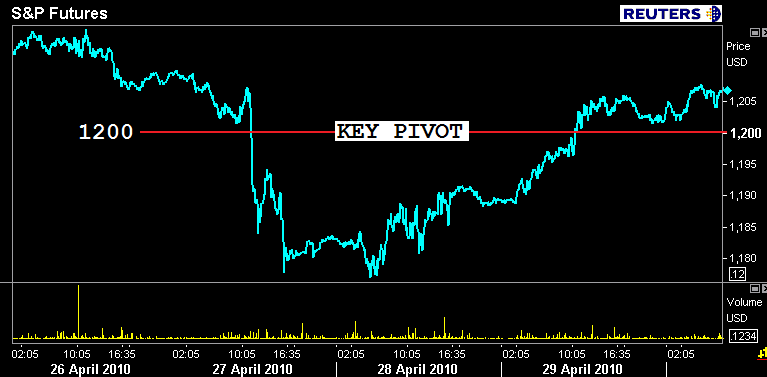

Ahead of the opening bell, Dow futures are up 13 points to 11,148 and S&P 500 futures are up 1.50 points at 1,206.75.

The 2 year Treasury note is flat at 99-31 yielding 1.008% and the 10 year Treasury note is -0-03 at 99-01 yielding 3.744%.

The US dollar index is down 23 basis points to 81.77. Commodities are also modestly upwards: WTI crude oil is up 32 cents to $85.49 per barrel, while Spot Gold is trading $7.97 higher to $1,174.82.