Calling the reform of the government sponsored enterprises (GSEs) Fannie Mae and Freddie Mac "the last piece of unfinished business from the 2008 financial crisis" the Mortgage Bankers Association today presented its proposal for the future of the housing finance system. The paper, which MBA says is the product of more than a year's work by a Task Force of individuals from MBA member companies, suggests and end-state model that ca also fulfill an affordable housing/duty to serve mission.

The group sets forth a lengthy list of policy objectives which include:

- Maintaining the liquidity and stability of the primary and secondary mortgage markets, and keeping the bright line between them.

- Replacing the implied government guarantee of the GSEs with an explicit one at the mortgage-backed security (MBS) level, backed by a premium-supported federal insurance fund.

- Protecting taxpayers with front-and-back-end credit enhancements.

- Establishing strong capital standards and regulatory powers.

- Creating a level playing field for lenders of all sizes and business models.

- Allowing the GSE regulator to charter new entities (Guarantors) to create competition by securitizing eligible single-and multi-family MBS.

- Preserving where possible the existing infrastructure.

- Strengthening affordable-housing policy consistent with sound lending practices.

- Ensuring that a robust private market can operate parallel and be complementary to the government-backed model.

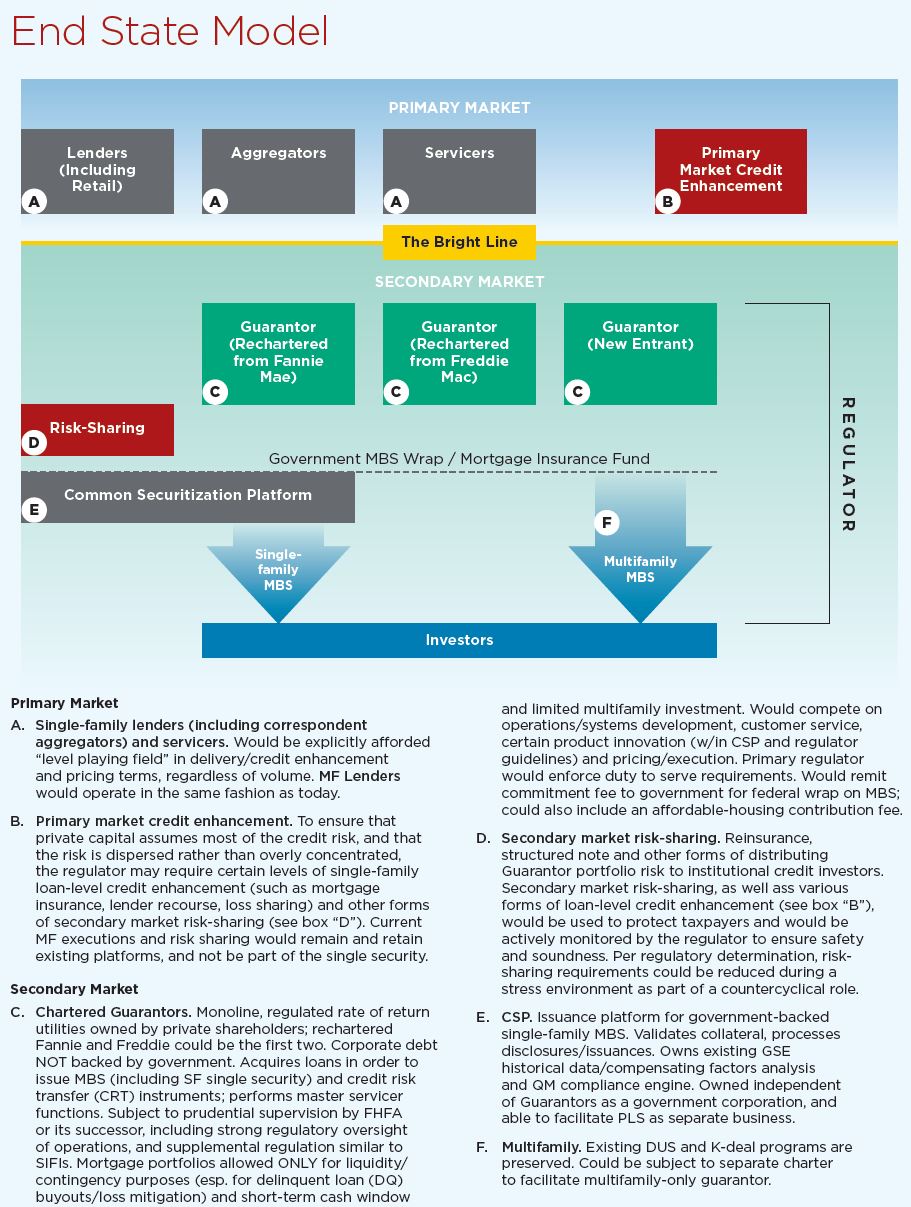

MBA says in many respects it has designed a system to preserve what currently works. Lenders would sell conforming loans into the secondary market by working with Guarantors. They would also continue to originate and securitize loans using other forms of guaranteed and non-guaranteed options including FHA, VA, and conventional loans held on bank balance sheets or securitized through private-label securities (PLS).

The process of selling conventional conforming loans would be similar to the current process. The rechartered GSE's and any new entrants would manage the credit risk on the pools and would issue the MBS and place the government guarantee.

The Common Securitization Platform (CSP) currently under development would issue a sole single-family MBS, most likely structured the same as the already proposed Uniform MBS (UMBS) but with an explicit guarantee. Investors will trade single-family MBS through a TBA market similar to the one today. Multifamily loans sold to Guarantors would utilize current executions such as Fannie Mae's DUS and Freddie Mac's K programs and perhaps other structures to be developed by Guarantors. The CSP would operate as a self-funded government corporation.

Guarantors would manage the credit risk on these mortgage through underwriting, retained capital, and through front-end and other risk sharing. Guarantor pricing would be tightly regulated by the regulator just as GSE pricing today is regulated by FHFA.

MBA believes there should be more than the two initial regulators, i.e. the current GSEs. Legislation would authorize the regulator, either the Federal Housing Finance Agency (FHFA) or a successor, to create competition (or the threat of it) through a process that would allow other entities to apply for and receive a charter under a process similar to that of applying for a national bank charter. It could be specific to a single family market, multi-family market, or both.

The regulator would be required to treat the system as a utility and consider the impact of new competitors on existing ones, on the relevant market, and on consumers. The guarantors would be monoline, regulated utilities owned by private shareholders, allowed to acquire single-family loans through both cash-window and MBS executions and multi-family loans through existing financing and other executions. MBA says the separation of the primary and secondary markets has been an important element of what had made the latter effective in providing liquidity and making mortgage credit available nationwide. The new system would preserve this "bright line" which is embedded in the GSEs' charters and specifically prohibits them from originating loans

Guarantors could hold a limited mortgage portfolio intended only for aggregation prior to MBS issuance, for delinquent loan buyouts, loss mitigation and limited multifamily purposes. They would complete primarily on operations and systems development, customer service, product innovation within set guidelines, and pricing and execution.

There would be rigorous capital requirements for Guarantors that could be met through a combination of their own capital and proven means of credit risk transfer which Guarantors would be encouraged to utilize. Lenders would maintain their current role in obtaining credit enhancements - PMI, recourse, existing multi-family risk-share mechanisms) while Guarantors would engage in risk sharing through reinsurance, structured notes and other mechanisms. The regulator could reduce risk-sharing levels during periods of market distress.

Guarantor-issued MBS would be backed by the full faith and credit of the federal government and supported by a federal mortgage insurance fund (MIF) built up over time by appropriately priced premiums paid by the guarantors. The MIF would cover catastrophic risk and would kick in only in the event of Guarantor failure after all layers of private capital had been exhausted.

Only if the MIF is exhausted would taxpayers be at risk. Should a bailout be required, future Guarantors would reimburse the Treasury and rebuild the MIF with higher insurance premiums.

The designated regulator would provide prudential supervision, set capital levels, and monitor and regulate target rates of return for the Guarantors designed to attract private investors. It would ensure fair and equitable access to the secondary market for all lenders without preferential pricing based on value, and ensure continuance of the bright line.

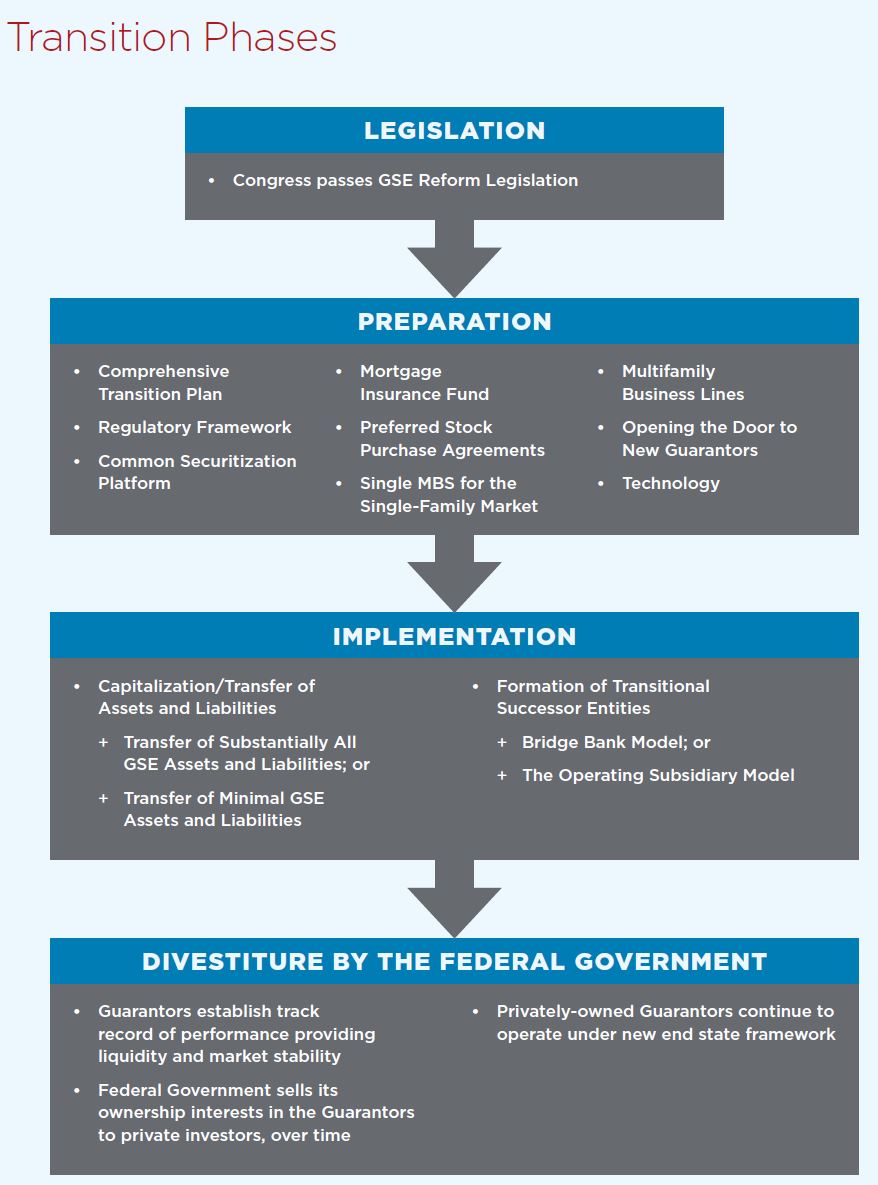

The Task Force says the transition to a new secondary market end state will be critical. It outlines a path which is designed to minimize disruptions to the existing housing finance system and bring the new system up to speed in a reasonable time. Their suggestions for a transition period would be to:

- Preserving the existing human capital and operational processes at both GSEs, supporting their emergence as viable Guarantors

- Transitioning to the new system over a multiyear period to avoid disruption and build required capital

- Reducing barriers to entry for new Guarantors to encourage competition

- Using FHFA and its existing legal authorities as a starting point, modifying the structure as necessary to achieve the objectives.

MBA emphasizes that only Congress can create this suggested secondary mortgage market. Its authority is required to change the existing charters for Fannie Mae and Freddie Mac and create the necessary guarantee for the mortgage-backed securities envisioned by MBA's proposal. It must also create the MIF to fund the guarantee, empower FHFA or another entity to regulate and charter the new Guarantors, and provide the legitimacy and public confidence necessary for housing finance reform.

The proposal also sees the need for a continuing mandate for providing affordable housing and sets out three critical missions:

- Providing responsible, sustainable access to credit for prospective homeowners;

- Providing liquidity for the development and preservation of affordable rental housing

- Improving liquidity for currently underserved markets.

To achieve these goals MBA recommends that the regulator periodically develop a comprehensive affordable housing plan against which to hold the Guarantors accountable, establishing both quantitative and qualitative affordable housing goals and assess an annual affordable housing fee on new business purchases of the Guarantors.